This is a free preview of a paid episode. To hear more, visit longtermstrategy.substack.com

Podcast: Play in new window | Download

Chronicles from a Caribbean Cubicle

New Thinking from Framework Consulting

This is a free preview of a paid episode. To hear more, visit longtermstrategy.substack.com

Podcast: Play in new window | Download

You are about to begin a fresh round of strategic planning. The team is eager, but before the retreat starts, you have a tricky decision. What length of time should your organization create a plan for?

Some already have strong opinions. The head of sales wants a 2-year plan. He needs the retreat to be short so he can go back to hitting his numbers.

At the other end of the spectrum, the V.P. of innovation and research wants some clear guidance on which technologies to pursue. The choices are wide, and a poor decision could doom the organization. She is thinking of a 40-50 year planning horizon.

They are both persuasive, but you need to make a choice. What are your next steps as the sponsor of the upcoming strategic planning retreat?

Fortunately, there is an approach that relieves you of duress. Given the importance of the planning horizon, get the team to make the choice during the meeting. How does this work?

First, explain to them why this is critical – the specific year and time elapsed (e.g., 2043, 20 years). It’s a critical one that deserves the input of all involved. As such, it should be crafted in real-time, face to face, but only when all the facts are on the table.

Therefore, the act of choosing the horizon should not be the first item on the agenda. Instead, begin by following a process to share pertinent information from all areas together in one place so that the team has a common understanding. During this preliminary session, remind the team that the next session will require them to choose a planning horizon. Ask them to keep this in mind as they review past performance and today’s issues.

This should actually help them remain hopeful. Why? Some of your company’s challenges probably only have complex, long-term solutions. In prior meetings, leaders gave up because they didn’t have enough time available. Now, they do.

When the subsequent session begins, explain the mistake of choosing a planning horizon which is too short or too long. Offer them the following two “warnings” to help pick the optimal timeframe.

Ask the team, “What happens if we choose a tiny horizon?” They may admit (after some reflection) that a 2 to 3-year plan will simply extend the past. Why? It’s only human.

They won’t say it out aloud, but people unconsciously prefer continuity and hate uncertainty. Our default mentality is to pick a predictable future. A short planning horizon keeps things comfortably the same.

But what about the power of a transformation? You should also remind them that if they don’t use time as a deep resource, they won’t create a Jim Collins-like Big Hairy Audacious Goal (BHAG). Such objectives are meant to inspire and uplift. They give meaning and add resilience, especially to younger staff.

Also, with a short planning horizon, key problems which need time will remain unsolved. Plus, you’ll also be missing important trends. For example, a 5-year planning horizon blocks you from seeing developments which take 7 years to mature. By contrast, if your competitors consider a longer time frame, they might include the trend in their thinking to their advantage.

Finally, aggressive executives love short-time frames because they see it as a way to force staff to work harder, and achieve results sooner. The problem is that some projects (like pregnancy) can’t be rushed. Don’t pretend that magic is real, or you’ll see employees merely going through the motions, doing the minimum.

Why? At its heart, short-termism is a synonym for selfish leadership. “My current needs trump your future needs.” It’s as if the team is also saying, “Instead of making difficult decisions now, we will leave them for you young folk in the hope that you still have time.” It’s the very opposite of sustainable business thinking.

Sometimes team members become true believers in long-term reasoning. They say “the more the merrier!” and call for a one-hundred year planning horizon. They may even cite examples of Asian organizations which do so.

However, you should take a look at your environment. Chances are, a planning horizon which is too long will mystify stakeholders who can’t relate. Instead of being inspired, they’ll become cynical.

Also, you might not have the resources or skills to plan too far out. Remember, whatever horizon you choose must be connected back to today.

Get your team to find consensus on the optimal time horizon in a healthy, real-time debate. It will set the stage for the success of your organization’s strategic plan.

Francis Wade is the author of Perfect Time-Based Productivity, a keynote speaker and a management consultant. To search his prior columns on productivity, strategy, engagement and business processes, send email to columns@fwconsulting.com.

You have heard the saying that “Culture Eats Strategy for Breakfast”. It has a ring of truth to it, but you don’t want to believe that strategic planning is futile – a victim of large, negative forces which cannot be overcome. But if it’s neither entirely right nor wrong, can we still use it?

The most depressing naysayers warn us that fancy plans can only go so far. Jamaican culture on a whole, or a specific corporate culture, will only allow so much change, but no more. But is this just a cynical way of looking at the world? Should it be discarded, or is there an element of truth that should be included in your planning for 2023?

After all, you don’t want to waste time shaping interventions meant to move the company forward, which could be doomed from the start.

In this context, what is culture made of? While there are many definitions, let’s assume that it comprises unconscious habits, practices, and routines. We all have them. And when we humans come together in an organisation, we can’t help but bring these elements, combining them into one.

For example, all companies have people who complain about being treated unfairly. Some leave their ruminations in the car park. Others spend most of their workdays kvetching to themselves. But our definition would focus on the complaints which are continually shared in workplace conversations.

By contrast, the occasional complainant, who resolves matters quickly, does not add to the culture. When a single problem is solved, it goes away.

This definition of culture is one your strategic planners should adopt. Why? Most teams I work with want to include some kind of cultural transformation in their long-term plans. Unfortunately, they lack expertise in this area. They only know enough to label organisations they have experienced from the past, judging some as superior, and others toxic.

However, they don’t know how to create a large-scale shift from one level to another. Without this expertise, their objective remains more of a hopeful wish than anything they can operationalise. To make things more concrete, here are some practical steps to take to forge the kind of culture that supports your strategic plan.

If your company hasn’t revamped its core statements in the last year, chances are they are no longer offering much guidance. In the worst cases, staff only use them to point out hypocrisy gaps…the places where your leaders are not walking their talk.

If you find yourself in this kind of situation, the standard advice is to undertake a refresh. Rather than driving up further cynicism and resignation, retire the statements and declare that they have done their job. Set up an effort to define new ones in light of a fresh strategy. Point out their purpose: to help accomplish a specific long-term vision.

This is Blue Ocean-style, opportunity creation at its finest.

But most leaders may still want the documents to be vague, echoing the tone of the ones they are replacing. Today’s best practice calls for a different approach. Instead of being ephemeral and high-level, look to define specific behaviours so they can’t be mistaken.

It may become clear as you do your planning that some of your corporate culture must be changed. For example, a culture of constant victimhood isn’t likely to be innovative and entrepreneurial…the behaviours your new strategy needs to succeed.

But these initial phrases are only clues. They aren’t detailed enough. Instead, take a deeper dive into the specific behaviours you want to change. Here, they need to pass the Video-Tape Test. If they can be enacted on film, then they are clear enough to be included in your strategic plan.

For example, a phrase like “responsibility” may fail the test because it doesn’t speak to a specific behaviour. By contrast, “I apologise to those I have wronged” is a specific behaviour which is undeniable.

It’s also one which can be trained, coached, measured and added into a performance system. As such, it becomes a tool to assist in accomplishing the strategic plan.

While you may group similar behaviours for ease of transmission, it’s important to be careful. Why?

The fact is, this isn’t about a change for its own sake. Instead, the planning team should see a clear cause-and-effect relationship between newly envisioned behaviours and critical elements of the strategy.

As such, these are carefully defined, culture-change projects designed to shift specific behaviours. Although such efforts are challenging, don’t allow them to languish or be eaten up by a toxic culture no-one supports.

Your company is thinking about creating a new role: strategy specialist. This person should support the entire strategy creation cycle and help produce a strategic plan with impact. But what exactly should be that person’s responsibilities? What uncommon value should they add?

The challenge of filling this position is unique. Why? Strategy is the main job of the CEO or MD. They birth a new plan in a retreat or offsite, then ensure it gets implemented effectively. The effort is meant to define the future of the organization and accomplish outstanding results.

In many companies, the top executive is the only person who is consistently looking far ahead.

As such, strategy specialists are playing specific support roles. Here are some unique activities they should undertake.

The best practices for crafting a strategic plan are constantly in flux. For example, if you are still doing a SWOT analysis in your planning meetings in 2023, it’s a sign of outdated thinking.

The most qualified person to manage and update the strategic planning process in your company could be the strategy specialist. They can do the research needed to uncover improvements and test fresh technology. This keeps the process running efficiently, engaging participants along the way.

The truth is, it’s quite hard to create a great strategic plan with a bad process. Some may think it’s a matter of personality, but I differ. While a “strong” leader can make a difference, this is a group effort.

A strategy specialist recognizes this fact and knows that a top quality plan needs a wide range of employees to implement them. What holds them together is a well-defined process and skilled facilitation.

When the planning cycle is over and implementation has begun, a strategy specialist needs to be wary of picking up the role of de facto project manager of “strategic initiatives.”

Instead, leave that role to the Project or Programme Management Office – PMO. This is, after all, their area of expertise. Alternately, focus on feeding the executive team with critical updates from outside. Here’s why it’s important.

Once a strategic plan has been completed, it’s not like adding another unit to a 1,000 home housing scheme. A carbon copy. Instead, it represents a compilation of brand new thinking.

As such, each strategic plan is built with a number of untested hypotheses, which themselves rest on a foundation of assumptions.

No-one can know for sure whether the hypotheses and assumptions are correct. But the strategy specialist must track whether they hold up as life unfolds.

In other words, long before an executive detects that there’s a huge threat to the current strategy, the specialist should have picked up early warning signs. In this sense, he/she is like a detective, scanning the horizon for bits of pertinent information which indicate a changing headwind.

It may be an industry trend. Or a fresh technology. Or a new government regulation. Perhaps a surprise competitor has emerged. These are all developments which threaten the foundations of the current strategy.

As such, they must be weighed and measured to determine if a revisit is necessary.

At the same time specialists monitor the external world, they should ensure that the plan is taking root in the organization.

Most companies have past horror stories about strategic plans which were crafted, and sounded good on paper, but never reached implementation.

There are a number of pitfalls which can occur. Some have to do with a lack of accountability. There are difficult, feedback conversations which just don’t take place.

Part of the reason lies with a manager’s missing skills. But he/she also lacks data.

I recommend you use the Balanced Scorecard to measure how well your strategic plan is being implemented. It can also be used to test the assumptions and hypotheses within the plan.

In both cases, the company’s leaders can see at a glance whether implementation is actually taking place. But are they required to watch the numbers this closely?

Absolutely. Every single strategic plan is intended to move the needle in an organization. This change occurs at the expense of prior habits and priorities. The battle to make these changes is real.

The specialist ensures that this progress is being made. They also raise a flag when not enough is happening to ensure success.

In summary, the strategy specialist role is an unusual one that most organizations have not identified clearly. However, every serious organization must perform these functions. Even if they are all conducted by the CEO, they should never be allowed to fall through the cracks.

This is a free preview of a paid episode. To hear more, visit longtermstrategy.substack.com

Podcast: Play in new window | Download

Subscribe to Chronicles from a Caribbean Cubicle Podcast podcast here on PodBean.

This is a public episode. If you’d like to discuss this with other subscribers or get access to bonus episodes, visit longtermstrategy.substack.com/subscribe

Podcast: Play in new window | Download

This is a free preview of a paid episode. To hear more, visit longtermstrategy.substack.com

Podcast: Play in new window | Download

You want to engage your staff around a bright, hopeful future. At some point in the past, a two-paragraph vision statement did the trick. But lately, it’s gone stagnant. What should you do to restore the inspiration it once provided? Should you change the words, or try something different?

You aren’t alone. Most companies have vague statements which sound a lot like each other. With phrases such as integrity and world-class being thrown around, you could probably swap your statement with another company’s without anyone raising a fuss.

The truth is that traditional vision statements have lost their potency, like a drug which has reached its expiry date. Today, there’s clickable inspiration available on Facebook, WhatsApp and TikTok, and your old statement just can’t compete.

But there’s a lesson here as well. In your next strategic planning retreat, you need to do more than build your vision of the future with a few flowery words. Here are some concrete steps to paint a vivid picture or end-vision employees find irresistible.

When you announce a traditional vision statement, if it has no year attached to it, folks in your audience do something interesting. Some believe it will be reached within a year, at most. Others assume 100 years. And if you leave this discrepancy in place, you force staff to eventually ignore it altogether. Why?

They see it as a farce. A con job.

And don’t complain that this wasn’t your intention. The world has changed and expectations have risen. Now, a vision statement needs a year attached to bring the kind of accountability which makes people sit up and pay attention.

If you already have a statement, but it’s “timeless”, launch a new effort. Don’t simply tag on a cool deadline. The way you picture the future must keep up with modern norms if you want it to be noticed.

Executives often make the mistake of believing that staff are motivated by financial results the way they are. Why? Most leaders’ rise up the ranks is a function of their ability to impact the bottom-line. Consequently, when they join the C-Suite, they are fluent in a certain language: the drivers of shareholder value.

However, employees aren’t interested as much.

Instead, a vision must be described in terms that do more than benefit the wealthiest 1%. Today, staff want to make a difference in the work they do and smart leaders develop empathy for this fact.

As such, the best executives describe holistic “visions” in detail. What do they look like? For a particular target year far off in the future, both quantitative and qualitative terms are used. They include as many as 20-40 descriptors and metrics. Together, these paint a rich picture of an end-game that pulls everyone in.

At the moment, Environmental, Social and Governance (ESG) goal-setting is in its infancy. For most companies, it’s a response to investors’ complaints.

As such, organizations are adding a layer of ESG tactics on top of their profit motives.

But most of these efforts are reactive and will miss the boat completely. Why? The ESG movement is actually a revolt against short-termism.

How did it come about? By focusing only on 5-year results, corporate leaders forced organizations to be profit-driven only. As such, other factors and impacts were overlooked.

It’s an easy error to make. For example, many international companies doing business in Jamaica have ignored their surrounding communities. That is until their executives have to be airlifted and escorted from the compound in the middle of a violent strike.

But there’s a solution. Take your company through the process of developing a 15-30 year vision along with a strategy to accomplish it. This will return the balance. Why? When you plan far into the future, you are forced to consider all salient factors.

However, if you try to squeeze ESG concerns into your five-year plan, prepare for your staff to decry its stupidity. They may not complain openly. But their reaction will be to seek inspiration elsewhere, where they can find some authenticity, e.g. church or social media.

Not that this is easy. Big picture, long-term engagement is not taught in business schools.

But it can be learned and coached into existence. And it can be programmed into your business by following a sound long-term strategic planning process.

The world is approaching a time when only holistic visions, which are big, realistic and balanced, will gain respect. Investors have begun to notice and so have employees. Don’t let short-termism ruin your leadership.

In your company’s strategic planning activities, you hope to make more than incremental improvements. Instead, your team dreams of brilliant decisions and breakthrough results. But are these a matter of luck? While fortune plays a role, Digicel’s introduction to the mobile telephony market is an example of a new competency: “category design.”

Christopher Lochhead would be proud of Digicel. He belongs to a cohort of content creators who call themselves the “Category Pirates.”

Responsible for several best-selling books, they argue that companies should not compete with other firms in existing categories. Instead, they should create and dominate brand new ones.

While this is far easier said than done, consider the example of Digicel.

Back in early 2001, cell phones in Jamaica were reserved for the privileged few. One would drop off a handset at a Cable and Wireless office for a few days, weeks, or months. The duration was unpredictable, and you needed to visit the building to see if the job was done.

You couldn’t help but notice employees who appeared annoyed at the intrusion. To the company, this was a minor operation…a nuisance. Many believed the local demand for this service was tiny. As a result, cell-phone signals were sporadic, perhaps offered in just enough locations to keep customers from complaining too much.

Looking back, it may seem that Digicel’s subsequent capture of 70% market share showed the power of competition. However, the company was actually doing something else your organization should consider: crafting a new category of service where no competitor existed. Here’s how they did it in spite of considerable risk.

1) New Technology

If Digicel were just another adversary, it would have used the same TDMA/CDMA technology C&W was using. Instead, it made a big bet on an approach Jamaicans had never seen: SIM-based, GSM.

To sign up, people would not only have to buy a phone but also a chip. Consequently, there were more moving parts. With the island’s low literacy rate, some believed people could not manage the sequence of actions required.

2) Island-Wide Coverage

If Digicel were merely competing with C&W, it would have fought to steal away high-value corporate and individual accounts in Upper St. Andrew. After all, they were existing users who could afford another monthly bill.

Instead, Digicel defined a new market. It offered service to some 75%+ of Jamaicans, only excluding the handful in the most remote locations.

This was a revolutionary strategy, and there was no guarantee it would work. Could ordinary people cover the added expense? Would they travel to a store (sometimes far away) to purchase a SIM card? How many were willing to learn how to use this new technology?

3) Customer Non-Care

C&W was well known for the poor service it offered to Caribbean customers. As a former part of the government, it appeared to be staffed with the worst of the former civil servants.

Digicel promised to offer a level of face-to-face service that was unprecedented. In the early days, it clearly delivered a stunning degree of customer care. Also, it undertook reward programs and prizes that gamified the business of mobile telephony for the first time. For several years, they offered cars as gifts for lucky customers during their annual Christmas promotions.

In retrospect, these three moves may seem to be obvious. But back then, it was a huge risk because each one relied on the other. Assumptions were made which could only be proven on launch day.

Yet, it still worked. Other islands in the region were envious as Jamaica rid itself of an unwanted monopoly…within days.

But this was no incremental improvement over C&W’s service…like yet another copycat pan chicken stand on Red Hills Road. It was a radical new strategy that combined fresh elements which had never been introduced to the Caribbean at scale.

Note that we Jamaicans love to “follow-fashion” each other, favoring the apparent safety of large numbers. It drove us to Olint and Cash Plus. Today it’s driving us to build high-end apartments on every available open lot.

It takes courage to bring about a new future, using only imagination and vision. But the good news is that this capability isn’t unique. This power is available to your organization.

But first you must understand that the essence of a breakthrough strategy is not duplication. Or competition. It’s “difference making” in which leaders define a new category in order to unlock fresh value.

Digicel did it, and so can your company in its next strategic planning session. I don’t intend to imply that doing so is easy. But there are proven methods for giving your creativity free rein that could lead to outstanding results.

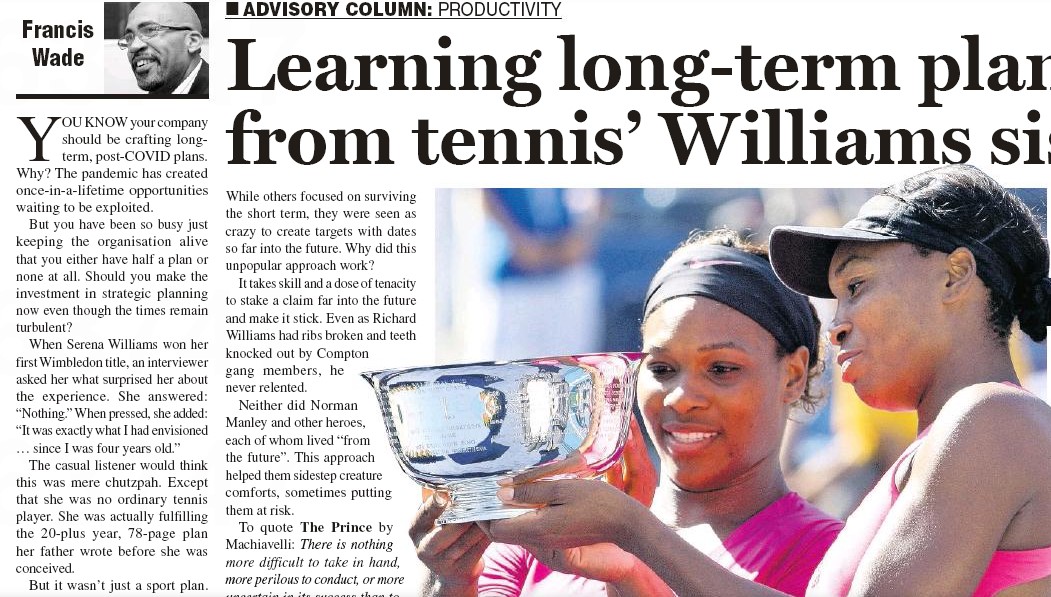

You know your company should be crafting long-term, post-COVID plans. Why? The pandemic has created once-in-a-lifetime opportunities waiting to be exploited. But you have been so busy just keeping the organization alive that you either have half-a-plan, or none at all. Should you make the investment in strategic planning now even though the times remain turbulent?

When Serena Williams won her first Wimbledon title, an interviewer asked her what surprised her about the experience. She answered – “Nothing.” When pressed, she added, “It was exactly what I had envisioned…since I was four years old.”

The casual listener would think this was mere chutzpah. Except that she was no ordinary tennis player. She was actually fulfilling the 20+ year, 78 page plan her father wrote before she was conceived.

But it wasn’t just a sport plan. The document covered Venus and Serena’s education, faith, family, responsibility, money…all aspects of their lives. It even inspired Naomi Osaka’s Haitian father to coach his daughter to the number one spot decades later.

Remarkably, the three champions have earned over US$180 million in their careers on the court. While some consider it to be all a matter of talent, the two coaches disagree. The success their daughters enjoy is due to advanced planning.

Like GraceKennedy’s 25-year plan and JMMB’s 23-year strategy, they were able to programme and accumulate small gains over time. While others focused on surviving the short-term, they were seen as crazy to create targets with dates so far into the future. Why did this unpopular approach work?

It takes skill and a dose of tenacity to stake a claim far into the future and make it stick. Even as Richard Williams had ribs broken and teeth knocked out by Compton gang members, he never relented.

Neither did Norman Manley and other heroes, each of whom lived “from the future”. This approach helped them sidestep creature comforts, sometimes putting them at risk.

Quote: “There is nothing more difficult to take in hand, more perilous to conduct, or more uncertain in its success, than to take the lead in the introduction of a new order of things.” The Prince, by Machiavelli.

But those who do come from the future inspire themselves to make changes. They declare a stated vision and live from it. This makes them two-headed: able to live today, and in the future at the same time.

If your organization’s executives shy away from putting themselves in harm’s way, it could be a lack of courage. But it may also come from the lack of detailed planning.

While most teams know how to spout vacuous vagaries to be “world-class,” they rarely have a 20-year plan to do so. The shortage of specificity lets them off the hook.

But the truth is, there are numerous ways to craft detailed multi-year plans which work, even without a shred of college education (i.e. like Richard Williams.)

One method successful companies use is to:

a. Convert the vision for 15-30 years away into details to be accomplished by a set deadline.

b. Translate qualitative details into an array of metrics.

c. Backcast metrics from the target year to today.

d. Schedule staggered projects to drive the metrics.

These techniques are challenging to employ during an offsite meeting. But the detailed plan produced can galvanize an entire company because of its credibility.

In retrospect, Williams argued that he needed a meticulous plan due to the uncharted waters he was navigating. No-one had ever done the impossible.

Furthermore, the role models in the sport at the time were succeeding wildly following the traditional approach. He refused to follow their lead, causing many to accuse Williams of ruining his daughters’ prospects. “Stop being selfish,” they said.

In retrospect, his wisdom is apparent. Countless others have entered the women’s tennis circuit and burned out. Only a tiny handful have played as long as the sisters have.

Some say it’s all a result of the Williams’ “character”.

Again, he argues differently. While his family has lots of it, he says that having a clear plan helped them weather and repel the criticism of experts who publicly questioned his sanity.

In other words, a good plan helped the family to stay the course. They found it easy to decide next steps – simply stick to the plan. After all, it was easier to do so than develop the “character” needed.

In this context, families are just like organizations. There’s no plausible reason to put off long-term planning if your company is committed to high performance. Instead, take the challenge seriously and accomplish the impossible.